Daniël Linders, Assistant Professor in Actuarial Science & Mathematical Finance, University of Amsterdam

Different approaches to price new exotic derivatives lead to different results. So which one should quants go for? Daniël Linders, Assistant Professor in Actuarial Science & Mathematical Finance, University of Amsterdam, argues, that quants shouldn’t need to choose in order to avoid bias in the decision. Here, Linders proposes a 3-step hedge-based valuation.

The ever-lasting expansion and innovation of financial markets led to product innovations in two directions. Exotic payoff functions entered the market place and risks such as longevity, climate change and pandemic risk are used to create a new kind of derivatives allowing investments in non-financial risks. With the introduction of these exotic derivatives, we abandon the existence of a replicating portfolio and therefore valuation becomes problematic and ambiguous. Different approaches are already explored, but they lead to different prices and their relation is not obvious. To avoid that the choice of the valuation approach becomes a subjective matter depending on taste, there is need for a unified valuation framework for complex hybrid derivatives.

Our starting point is a contingent claim depending on different types of risks. For example, an insurance-linked security (ILS) is a derivative whose payoff depends on a catastrophic loss event. Pandemic bonds provide a payoff which depends on a pandemic event whereas natural disasters such as hurricanes and tornadoes can be used to define catastrophe bonds.

Quants can use the help of actuaries when pricing such complex products. The ILS contains typical actuarial features. Actuaries possess different skills than quants. Whereas quants start a valuation armed with risk-neutral expectations and hedging portfolios, actuaries rely on real-world expectations, risk measures and premium principles. In this paper we unite the quant and the actuary and bundle their powers to develop a unified framework for the valuation of derivatives that depend on financial as well as non-financial risks.

There are three main risk categories: financial, systematic and actuarial risks. A hybrid claim is a claim that is a combination of these different type of risks. The valuation of a hybrid claim should correspond with the amount of capital needed such that one can set up an adequate risk management strategy for the hybrid claim. The problem is that different risk types require different risk management strategies and therefore also different valuation approaches.

A financial claim such as a vanilla call or put option, depends on traded assets and quants use replicating portfolios to determine the price. Actuaries, on the other hand, developed a valuation framework for insurance claims, such as life annuities, which is based on diversification. A systematic risk is a risk that cannot be managed by diversification nor can it be managed by a replicating portfolio. For example, inflation impacts each policyholder in the same way and therefore adding more policyholders to your portfolio will not have the desired risk-reducing effect. Systematic claims are managed using large capital buffers that serve as a cushion for adverse shocks.

The complexity of hybrid claim valuation is often circumvented by assuming simple payoff functions and independence between the different risk types. Another simplifying setting is decomposing the claim in a financial, actuarial and systematic part and then assuming an additive valuation where each part is valuated using an appropriate valuation principle. However, these assumptions are by far realistic. Our unified framework allows for more general settings, but at the same time incorporates the existing methods.

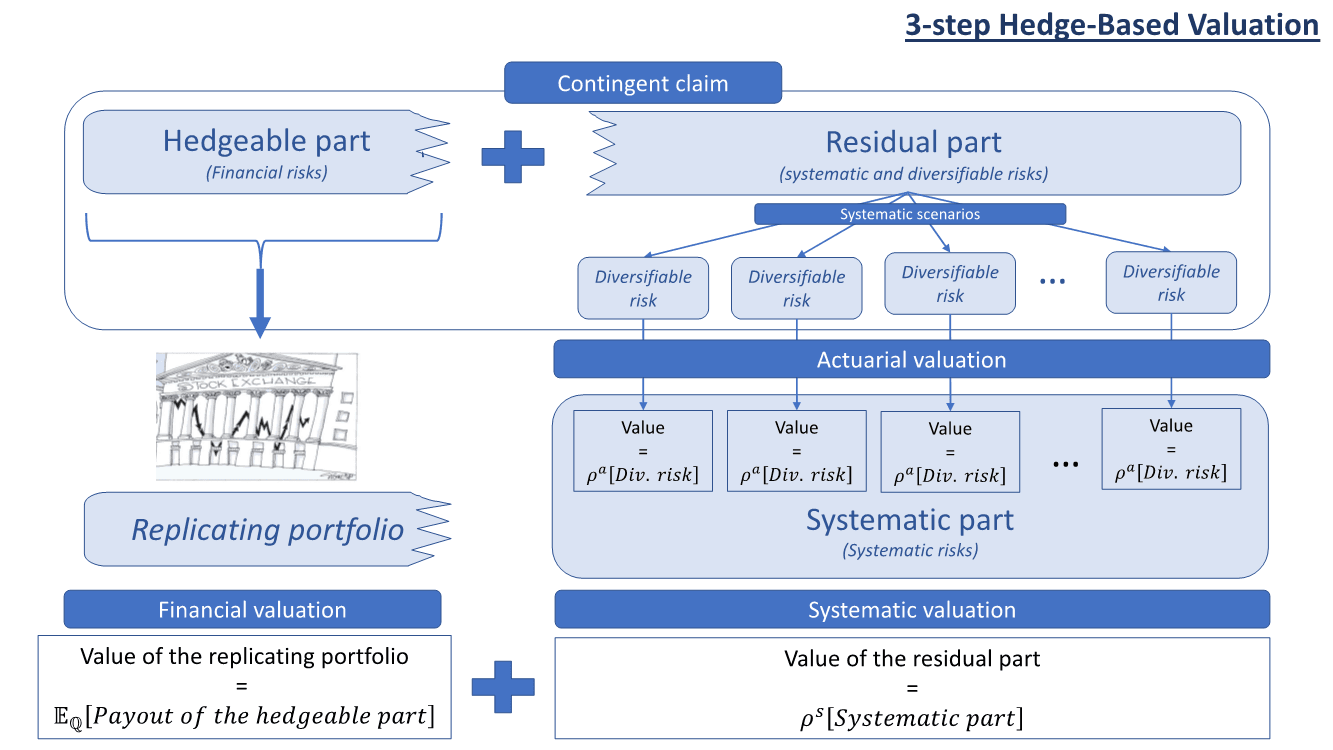

The aim is to determine a unified framework for the valuation of hybrid claims that takes into account the differences between financial, diversifiable and systematic risks. We call our valuation the 3-step hedge-based valuation. Figure 1 gives a schematic overview of the valuation steps.

The valuation is called ‘3-step’ because there are 3 steps in the valuation: there is a financial, an actuarial and a systematic valuation step. The valuation is called ‘hedge-based’ because we first search for the best replicating portfolio. The valuation of the claim relies, as much as possible, on available market prices. Therefore, we look for a replicating portfolio that covers the payout of the claim as much as possible. The result is a decomposition of the hybrid claim in two parts. The hedgeable part, mimicked by the replicating portfolio, and the residual part. The quant deals with the valuation of the hedgeable part. The actuary should determine the value of the residual, non-hedgeable, part.

The main risk drivers of the residual part are the actuarial and the systematic risks. Since the actuary is most familiar with the actuarial risks, we consider different systematic scenarios. Each scenario corresponds with a certain outcome of the financial market and a particular systematic shock. The remaining uncertainty then only comes from the actuarial risks. The actuary can select an appropriate actuarial valuation principle such that we end up with a set of actuarial values for the residual part of the claim, each value corresponding with a particular systematic scenario. In the third, and last step, we determine the value of the residual part as the actuarial value that corresponds with the worst-case systematic scenario.

Figure 1: The different valuation steps for the 3-step hedge-based valuation principle.

Pension liabilities are combinations of traditional insurance benefits and traditional financial guarantees. For example, a pension liability can provide a lifelong annuity, but the annuity payout depends on the performance of the stock market. Additional guarantees are embedded to ensure an adequate annuity payout. Having a solid and reliable valuation framework is of utmost importance. Indeed, the consequences for the society can be disastrous if insurance companies become insolvent and long-term guarantees cannot be met. The 3-step hedge-based valuation provides a new valuation framework for pension liabilities. It provides the flexibility to control the valuation approaches for the different risks separately.