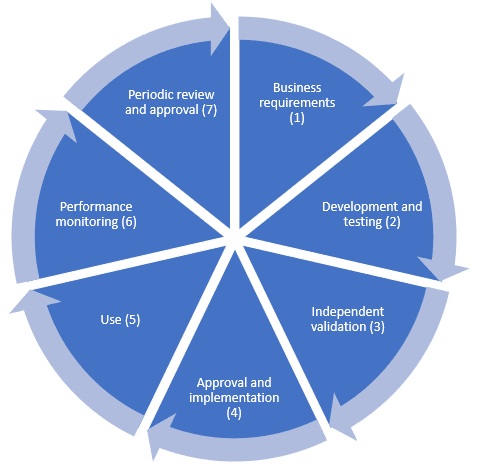

As first step, it is important to consider the stages of the model lifecycle (see figure 2) and map the required controls on them.

Figure 2: Model lifecycle

The below questions can help to identify the necessary controls for each step:

In order to establish a control framework for an MRM, there are some of the key elements to take into consideration:

Policy and procedures are essential to establish key points such as model definition, materiality etc.

Allocation across the usual categories as developer, validators, user, and approver.

This is a main pillar of the model risk framework as it contains critical information such as model owner, weaknesses, validation due date etc.

They are used to assess and monitor the model materiality according to the risk appetite and business model of the financial institution.

Verify the feeding workflow between and among models to determine the parent-child relationship.

Different teams use different releases of the same model.

Check on data quality and integrity to verify the reliability and validity of the information and whether it's eligible to be used to feed a model for the intended purpose.

They determine the equilibrium between the key areas of MRM (e.g. development vs validation) because if there is as imbalance, the MRM cannot achieve its scope.

They are essential to norm the steps of key actives such as model development, validation etc.

Drilling down in the validation stream, it is important to select the type of testing appropriate to the materiality of the individual model.

It is a key element of the model development (often ignored at this phase of the model lifecycle) and vital to evaluate if the model is working as expected or if any corrective actions are required as described in detail in the next part of this article.

The outcome and associated guidelines provided by Targeted Review of Internal Model7 (TRIM) published by the European Banking Authority (EBA) represent a robust reference for the financial institutions who desire to enhance the above elements of the MRM mainly for the internal models.

Obviously, a robust model risk framework offers many benefits including the following8: