What will be the top trends of 2021?

For our 2021 annual technology trends whitepaper we include trends from analysts covering the physical security technologies and critical communications industries.

Coming out of 2019, our 2020 whitepaper forecast a continuation of positive growth. The worldwide physical security equipment market grew by over 9% in 2019, with some regional markets, like India and Southeast Asia, expanding even more rapidly. However, against a backdrop of global industry disruption from COVID-19 and continued trade disputes between the US and China—the world’s two largest economies and also the two biggest players in the physical security market—the physical security equipment industry experienced significantly slower growth of less than 2% in 2020.

Despite many technologies experiencing negative revenue growth in 2020, Omdia is positive on the outlook for 2021. Optimism surrounding new technology developments, coupled with markets opening up and fewer restrictions on peoples’ movements later in the year as vaccination programs take effect, are expected to drive worldwide growth of 8% this year.

So, what will be the big stories in 2021? Video-centric IOT, AI-driven hybrid VSaaS solutions, and frictionless biometrics are just some of the trends discussed in our eleventh annual white paper on trends for the year ahead.

The predictions on the following are to provide some guidance on opportunities across security technologies in 2021:

If you would like to speak with one of our analysts on any of the topics covered in this paper, or to discuss our service offerings, please contact us. Oliver Philippou, Research Manager – Physical Security Technologies

Navigate directly to any of the trends using the links on this page or using the arrows. on the right side of the page. If you wish to download the report, you can do so via the Contents menu in the top left corner.

Find out more or contact us >

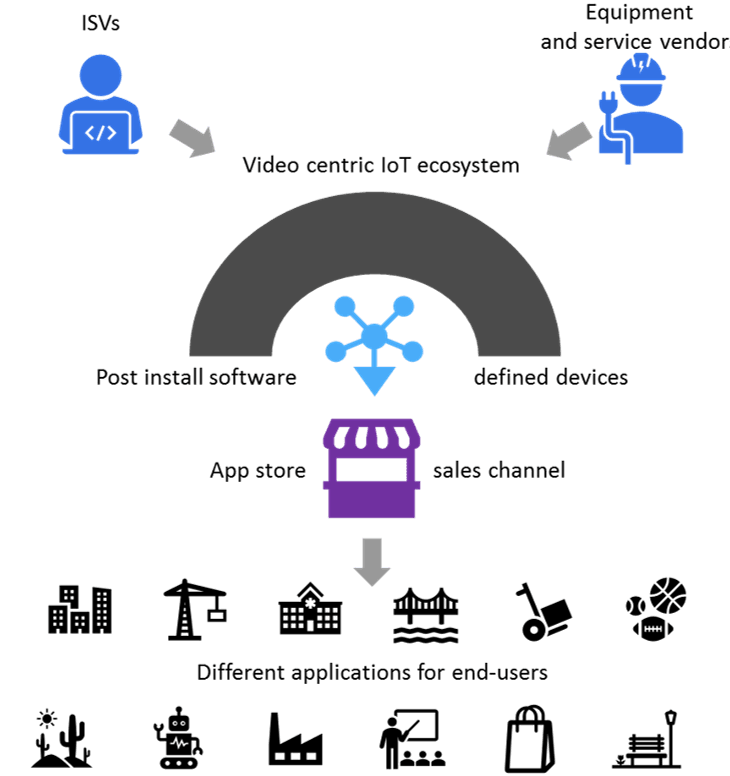

As video surveillance goes “beyond security,” video-centric IoT is a concept being increasingly marketed. Video-centric IoT platforms are built on the concept that intelligent cameras can use the latest video analytics to provide multifunction metadata rather than having several independent sensors, each providing data for different applications. Additional sensors and devices are also integrated, yet, cameras as a keystone sensor and an inbuilt proficiency in managing video data offers platforms architected in this way a potential advantage over other platforms which may add in cameras as just another sensor. Currently, the trend of video-centric platforms is manifesting itself in the development of camera-first ecosystems with dedicated device operating systems. These also center around cameras as multiuse sensors with “software-defined” capabilities being offered via application developers. This isn’t new, but the “appification” of cameras via app store models that offer less friction than previous ecosystems is a development to watch. Competing ecosystems have a range of “openness.” Some offer a range of hardware and software apps from third parties, some only offer software from third parties, and some offer everything from a single vendor.

To take this concept into the realm of true IoT ecosystems, it is challenging to see how a single vendor could offer a full range of IoT devices, thus a degree of “openness” is likely required to achieve a dominant global video-centric IoT platform: A video-centric IoT platform which can aggregate data from surveillance cameras and a range of different sensors in order to serve a wider range of applications “beyond security.”

In both the 2019 and 2020 trends whitepaper, a key discussion point was the development of advanced system-on-chips (SOCs) for analytics at the edge—in particular, for deep learning analytics at the edge. In professional video surveillance applications, Omdia expects the increased deployments of AI on camera in 2021 to continue.

As with most new technologies, AI at the edge has been focused on the high-end of the camera market. But in 2021, Omdia expects this technology to increasingly make its way into the mid-market. Omdia does not expect AI-based cameras to significantly penetrate the low-end market for several years. Announcements in 2020 regarding developments of AI cameras were made by software vendors, camera manufacturers, and semiconductor companies alike. A significant announcement of note was made by Ambarella. In November 2020, Ambarella announced the development of the new CV28M chipset. An addition to the CV family of SOC’s. This chipset’s performance and price would be more moderate than the CV22 and CV25 product offerings.

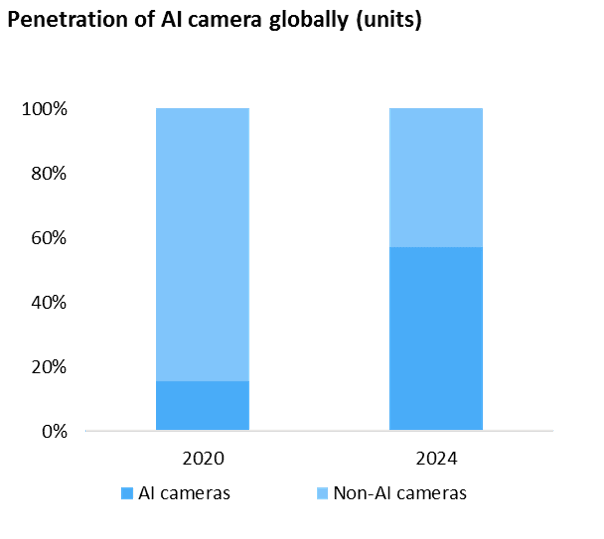

Omdia estimates that 8% (2% globally excluding China) of all network cameras shipped in 2019 were AI cameras, increasing to 16% globally in 2020. However, development of image processers, and the release of AI cameras by leading equipment manufacturers, is expected to drive the development of this market. In 2024, the percentage of surveillance cameras shipped which are AI cameras is forecast to grow to 58%, meaning that this technology will be available to large parts of the mid-market sector.

China continues to drive the growth of global video surveillance market

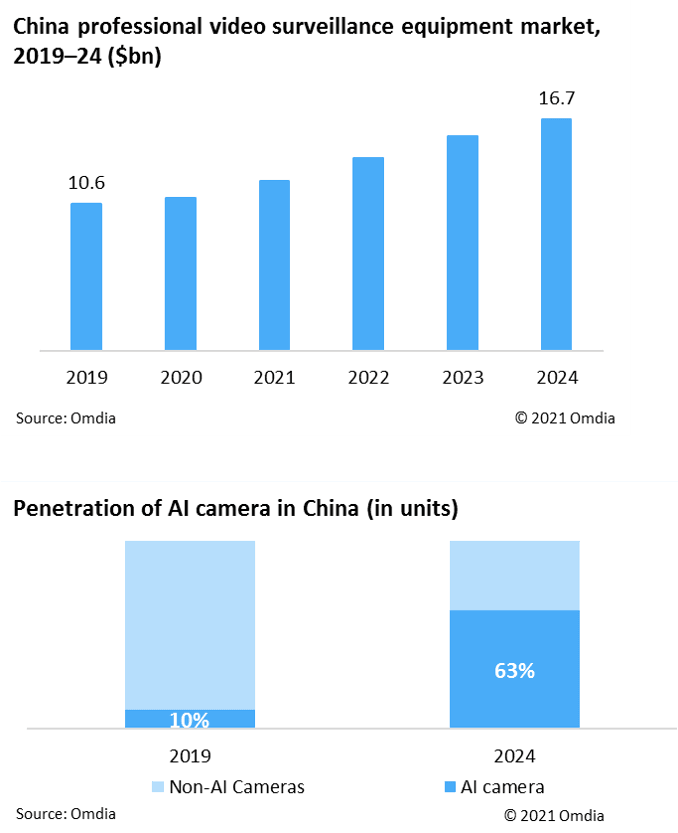

It is estimated that Chinese professional video surveillance equipment market revenue reached $10.6 billion in 2019, accounting for 48% of global revenue. Although the Chinese market is forecast to grow only 4.1% in 2020 due to the impacts of coronavirus, it is forecasted to grow at a five-year CAGR of 9.5% to $16.7 billion in 2024. The government’s new infrastructure construction plan is a major driver of demand in China. Market growth is also bolstered by fast adoption of advanced technologies such as video analytics software and underlying IT infrastructure.

AI analytics along with supporting infrastructure will boom

With a greater number of cameras deployed, storage, analysis, and the ability to search video becomes increasingly challenging. With the help of AI video analytics, object classification and video search can be faster and easier. AI metadata can be generated via analysis completed onboard the camera (the edge) or at the server/recorder (the core), often a combination. Omdia estimates that 10% in 2019, and 19% of network cameras shipped in China in 2020 were AI cameras (embedded with deep-learning analytics). The penetration rate will grow to 63% by 2024. Although AI is moving to the edge quickly, video analytics processed at the center will still show robust growth. This will drive the demand for ICT supporting infrastructure (including server, HCI, and external storage). Omdia forecasts that the supporting infrastructure market will on average grow 11.8% annually to 2024.

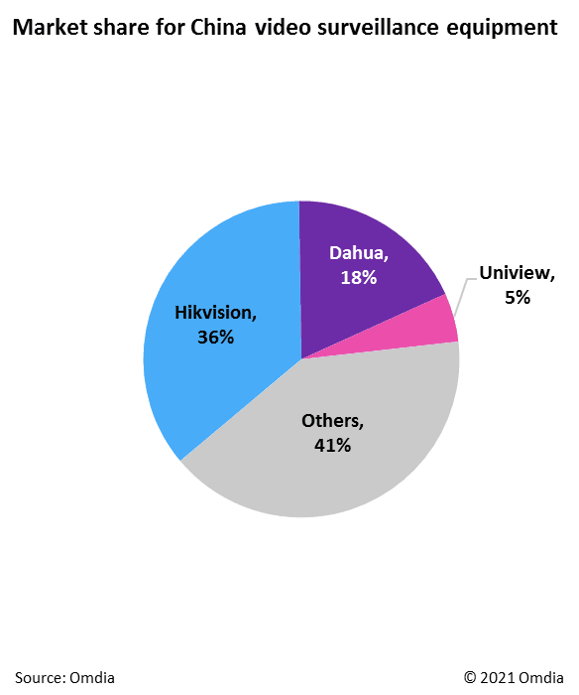

The Chinese market gets concentrated Although there have been some significant new entrants into the video surveillance market in recent years—AI startups such as SenseTime and internet giants such as Alibaba in particular—the supply base for Chinese professional video surveillance equipment is gradually becoming more concentrated. The top three largest video surveillance vendors accounted for 59% of Chinese video surveillance equipment revenue in 2019. However, new entrants with expertise in AI, big data, and cloud are gaining shares from smaller traditional video surveillance vendors. A major factor is the adoption of the advanced technologies in which these vendors have a background.

Going forward China will continue to be the largest market for video surveillance equipment, with the largest installed base of cameras. The investments in the future will concentrate on the utilization of video footage generated by the large installed base. As cameras become an integral part of IoT networks, an IoT system that can extract useful information from cameras and sensors, analyzing inter-relationships among data, and generating actionable insights, will provide significant value to stakeholders. AI analytics, along with the supporting infrastructure market, will continue to see fast growth in the coming years.

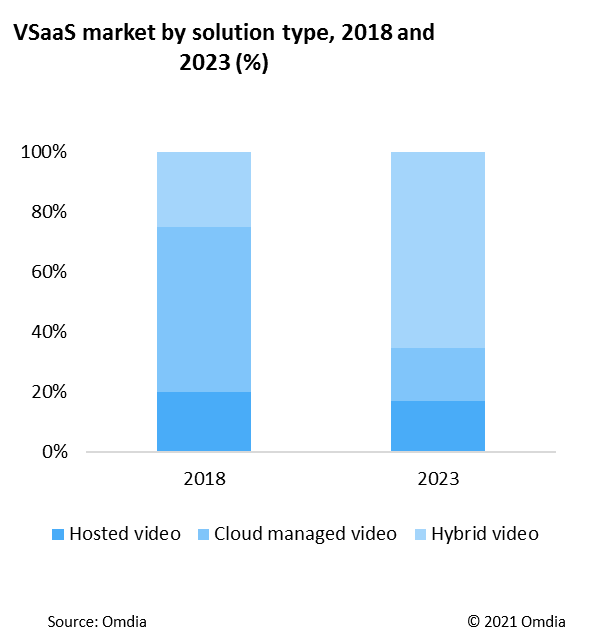

Hybrid solution could be an efficient way for PSaaS, as AI penetration grows in the physical security market As AI is increasingly adopted by the video surveillance market, end-users’ requirements are also becoming increasingly more varied. In these cases, a powerful platform that offers both central management and integrates with intelligent applications is becoming increasingly essential. Currently Physical-Security-as-a-Service (PSaaS) vendors such as Cisco Meraki already offer such solutions. However, bandwidth constraints continue to limit development of PSaaS solutions. Despite telecommunications companies continually improving network speed, this focus has been on improving download speeds rather than upload speeds. Moreover, there are an increasing amount of IoT sensors and high-quality videos that have enabled better analytics applications, but which are also challenging to upload this video and data to the cloud. A hybrid solution could be the most efficient way for a better end-user experience. Usually, it would be smart edge with cloud windowpane, which means processing is on premise, while storage (or parts of storage) and management are in the cloud. This mode could offer greater choice of applications, compatibility, lower burden of bandwidth, management of storage, and more efficient use of analytics. Specifically, in China, this hybrid solution also fits the needs of fixed assets for some government projects. Omdia forecasts that revenue from hybrid VSaaS will grow the fastest, with a CAGR of 30% from 2019 to 2024.

Facial recognition and frictionless fingerprint readers will fuel the growth of biometric technologies in access control systems A frictionless biometric reader is a device that is capable of scanning and processing a user’s biometric data without requiring the user to pause and initiate physical contact with the device. Nearly every facial recognition reader, most iris recognition readers, and a newly emerging class of frictionless fingerprint readers installed in access control systems today are defined as frictionless biometric modalities.

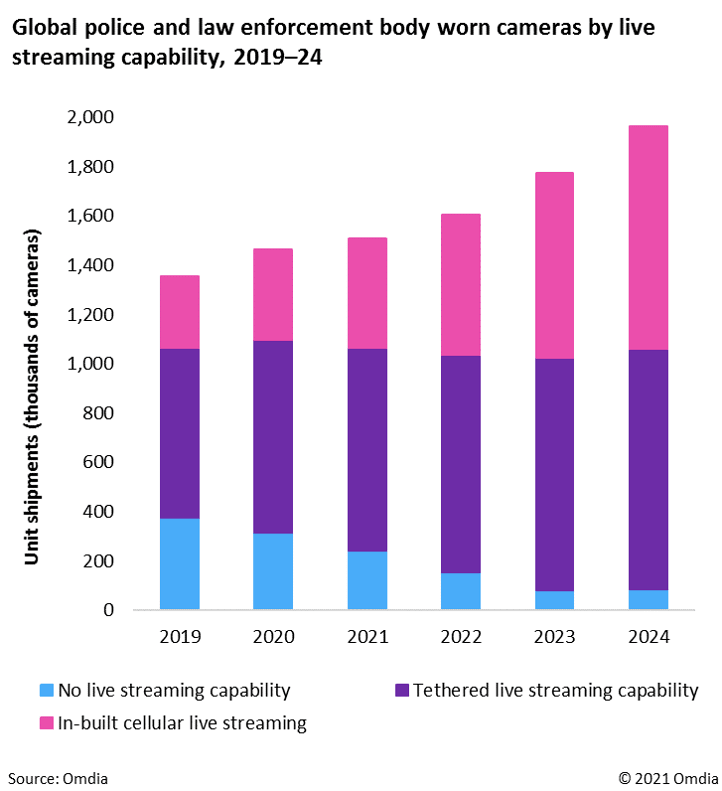

The potential total addressable market for private security dwarfs that of law enforcement. Feature set expansion for body worn cameras, including live streaming capabilities and location-based services, are set to spur adoption of body worn cameras outside of the traditional law enforcement applications in which the industry began. The body worn camera industry is still in its infancy, with product specifications and customer requirements continuing to evolve as the way the technology is used continues to be refined at an organisational level. In the US alone, the number of private security guards outnumber police officers almost two-to-one. Even this imbalance does not include all of the other non-law enforcement roles—ticket inspectors, traffic wardens, health inspectors, door staff, etc.

Even outside of these traditional enforcement type roles, new users are emerging in the form of retail staff. In July 2020, the Co-op, one of the largest food retailers in the UK with more than 4,000 shops, began supplying frontline store staff across 250 stores with body worn cameras in response to a “crime and violence” epidemic. They plan for a wider roll out to some 600 stores. The body worn cameras deployed can stream live video, when requested, to a remote monitoring station. Live streaming via LTE and GPS integration in body worn cameras are the two largest drivers of the feature set expansion occurring in body worn camera products today. It is clear that alongside feature set expansion for products also comes total addressable market expansion for the industry.

Mobile network operators emerge as key partners for public safety mission-critical networks The model for national mission-critical LTE networks has been in gestation since the US battle for the D-Block culminated in establishing the FirstNet Authority in 2012. Efforts in the UK, Korea, and the UAE embraced a diverse set of approaches with varying degrees of government network ownership. In 2021, paths are converging upon public/private partnership models, as exemplified by the US government's 2017 contract with AT&T, the UK's contract with EE, and Finland's deal with Elisa. Subsequent national decisions will leverage the mobile network operator's geographic coverage advantage and 3GPP mission-critical feature specification to cost-effectively deliver services.

Smart public safety agencies are a key element of smart and safe cities of the future and the present COVID-19 has forced a rethinking of traditional ways of working, and has and forced many businesses to rethink their business models. In the public safety sector, the pressure of the pandemic has put a significant strain on daily missions of public safety agencies. However new technologies are promising to increase the efficiency and effectiveness of their daily missions and the stress of the pandemic is likely to speed up their adoption. IoT technologies promise to create smarter public safety forces, with wearable devices keeping a watchful eye on the well being of fire fighters and police officers, while smart sensors and cameras deployed in wild forests work to warn of impending fire before they engulf large swaths of areas and threaten nearby livelihoods.

Crime solving in the 21st century hinges on digital evidence. However, with the growing number of new sources of data such as body worn camera feeds and ever-expanding city surveillance systems, it is a challenge for investigators to make the best use of all of these resources. Currently, detectives often have to log on to a dozen systems and manually search for connections between cases, which wastes time and increases the likelihood that crucial evidence will be missed. Scalable, cloud-based digital investigation and evidence management solutions solve these problems by consolidating silos into a single log on, and by providing built-in evidence collection, crowdsourcing, content analytics, visualization, and evidence sharing tools to make investigators more efficient and effective crime-solvers. Drones are becoming a key partner of police forces. Their adoption is fast growing, and the latest use cases continue to expand beyond crime or fire scene monitoring. When Beyond Visual Line Of Sight (BVLOS) operations become mainstream, a whole new range of public safety missions will open. Existing technology is just about ready to support initial widespread BVLOS missions; however, the biggest barrier has been the strict regulatory environment. The regulatory environment differs between countries and regions and many countries are at opposing spectrums of adoption of BVLOS as a concept for public safety work, but new regulation breakthroughs are expected in the very near future. Adoption of machine learning to support BVLOS modes will serve to align concerns over safety of extended-range, autonomous flights.

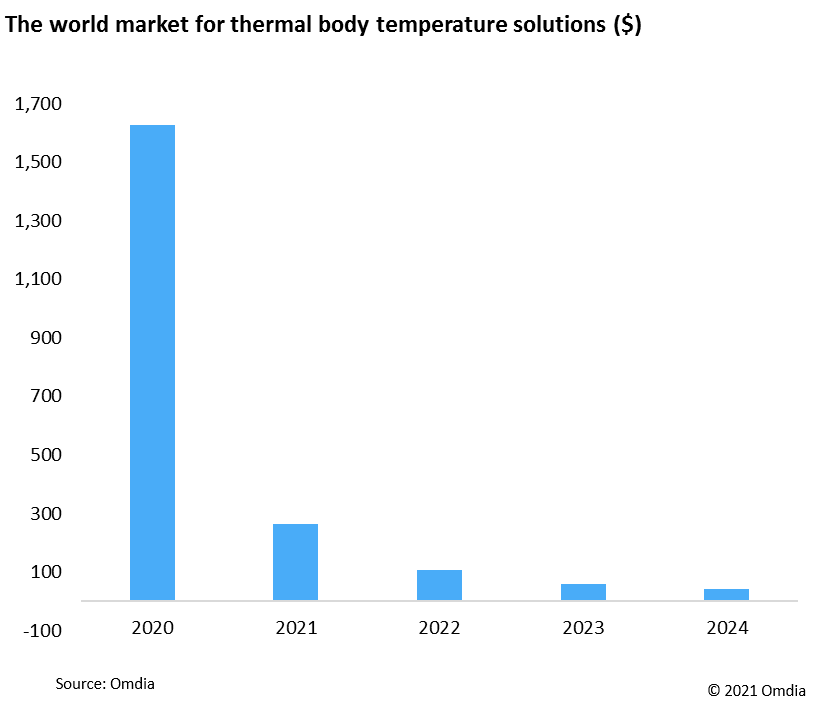

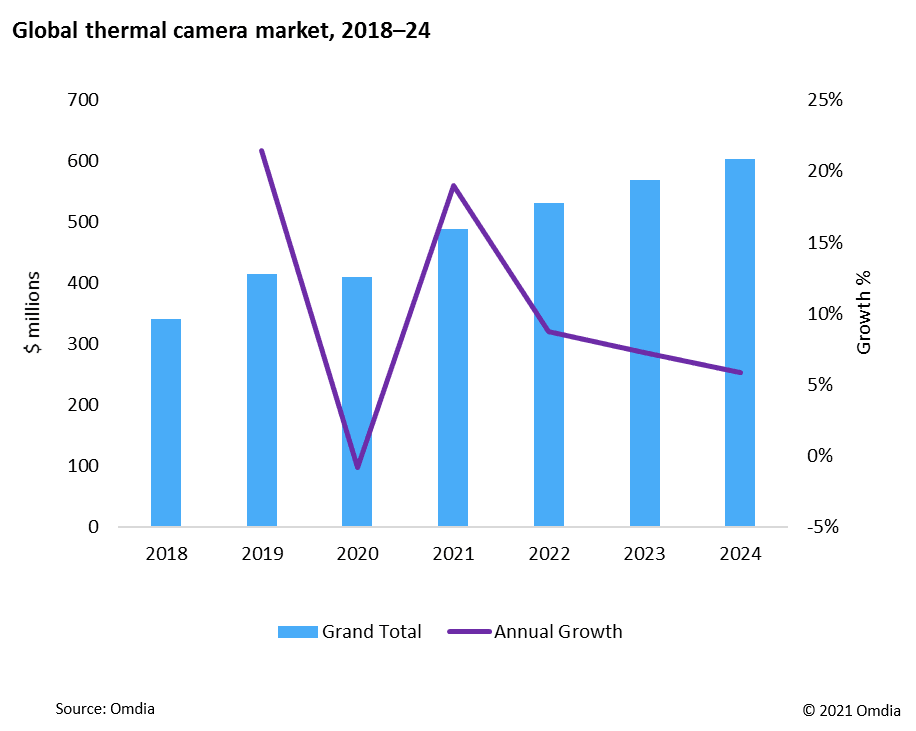

Thermal cameras used for body temperature screenings have emerged as a new (but temporary) market With the COVID-19 pandemic disrupting the global economy, businesses have searched for alternative measures to get back to business as safe as possible. One of the solutions has been measuring the body temperature of employees and customers. Thermal camera suppliers have produced infrared solutions that detect elevated skin temperatures. These solutions are particularly popular in airports, factories, retail, and government facilities. Infrared thermography can detect elevated skin temperatures, which may indicate the presence of a fever. When followed by a screening with a medical device, the use of an infrared camera as an adjunctive diagnostic tool may help contain or limit the spread of viral diseases such as bird flu, swine flu, or COVID-19. Research has shown that the corner of the eye—the region medially adjacent to the inner canthus—provides a more accurate estimate of core body temperature than other areas of skin. This is because skin at the canthi is thin (decreasing insulating effects), less exposed to environmental factors, and directly over major arteries, which increase blood flow and heat transfer. Omdia classifies the market for thermal cameras for body temperature as a completely different market than the one for perimeter security. This market is projected to not be long lasting, and will only have significant revenue through 2024.

AI in perimeter security cameras has become crucial for object classification AI adoption for thermal camera imaging has gained momentum in the last couple of years, and is expected to become an industry standard throughout the forecast period. Deep learning allows for cameras to classify what type of intrusion it is (car, person, animal) and allows for faster deployment if necessary. This process eliminates the need for a host system for classification task. Another advantage of AI for thermal cameras is the accuracy of the location where the intrusion was noted, and its movements. The system can also determine what kind of intrusion it is based on the patterns showed by its movement. Pan-tilt thermal cameras are usually redirected in the position of an intrusion by a complementary perimeter security sensor like radar. When the radar system detects an intrusion in the perimeter, it automatically directs the camera towards the object for video confirmation, recording, and classification.