New Ag International JUN/JUL 2020

Nestled on the banks of the Murray River, Albury makes a good location for an agricultural producer serving the eastern cropping belt of Australia. The city is also on the main highway that heads out to the agri-heartlands of Western Australia.

New Edge Microbials (NEM) is based on the northern outskirts of the city, a short distance from air, rail and road terminals – also handy for shipping inoculants out west. The company’s production facilities comprise a total fermentation capacity of 45,000-50,000 litres.

Founded by Sandy Montague in 2000, NEM is owned in the majority by the Zinga and Barlow families, and also counts among its shareholders the company’s founder, Sandy Montague, the company’s chief operating officer Grant Kelson and the company’s strategic adviser, Lion Capital, Melbourne. The company has 20 full time employees, which can increase to 40 depending on the demands of the season.

NEM Managing Director Ben Barlow (left), with his brother Luke Barlow who farms Woodfield Estate.

Peat products The core business of NEM is the production of rhizobium inoculants in deep-tank fermentation.

“Eighty-five percent of our business is derived from that,” says Barlow, who comes from a farming background and an earlier career in corporate finance. “The product is independently tested by Australian Inoculants Research Group (AIRG), a group within the NSW Department of Primary Industries (NSW DPI) Soils Unit, giving the farmer a high level of confidence that it has been independently ticked off.”

In the Australian market, the dominant formulation is peat. Peat-rhizobia inoculant can be applied in a variety of ways. Typically, it is added to water to create a slurry, which is then applied to the seed as a coating. A peat-rhizobia inoculant can also be used in water injection systems that apply directly to the seed furrow. And, it can be applied as a dry crumble directly into seed bins for seeding.

Within the Australian cropping sector, peat is the dominant formulation accounting for 65 percent of the sown area, other formulations treat the balance, while the pasture market is dominantly treated by pasture seed companies, according to Zinga.

The strains used to make NEM’s NoduleN™ peat legume inoculant product are supplied by the AIRG. They are selected for being the most productive for effectiveness, host range, field performance, soil persistence, genetic stability, fermentation, inoculant survival and most important nitrogen-fixing capabilities. The high levels of humic materials found in peat provide nutrients and store moisture to help the Rhizobium bacteria establish.

Daniel Zinga, NEM Director, sales and product development.

NEM also has a highly concentrated formula that is unique for the Australian rhizobia industry – EasyRhiz™ – and that comes in a vial. This provides users with an inoculant formulation that is dormant, with minimal storage requirements. The most common use for the product has been with farmers who are equipped with liquid injection systems, though it may also be used as a seed inoculation treatment in moist soils.

In addition, the company produces a liquid inoculant for the soybean market, though this crop is at a smaller scale in Australia versus other parts of the world.

The remaining part of the business involves the production of other bacterial strains, such as Bacillus, Pseudomonas, Streptomyces and the fungus Trichoderma, for various applications related to improved nutrient uptake in crops other than legumes. Like all NEM’s products, they are produced under deep tank fermentation. NEM also has the nitrogen fixing Azospirillum in its library and is under product development for the local market.

NEM has designs to enter the growing biocontrol market. It has the capability in its fermentation although, with any control or suppression claims, products are required to go through the registration process with the government’s regulatory agency, the Australian Pesticide and Veterinary Medicinal Authority (APVMA).

“The market is interested around soil health and integrated pest management, and the consumer is demanding softer products,” says Barlow, noting there is good support for Bacillus products in the Australian market. “The Australian market is very cautious if you do not go down the regulatory path or have strong data from field trials.”

No strain, no gain The growth in the inoculants market is very much reflected in NEM’s own growth profile.

“It’s been tremendous,” says Zinga, whose career has spanned roles from agronomy to working with Becker Underwood and BASF. He notes BASF’s take-over of Becker Underwood was hugely disruptive to the market, on top of its re-entry to the Australian market in 2014 to manage the company’s crop protection business.

Zinga’s appointment to NEM in 2014 appears good timing. The smaller, more nimble NEM has been able to build an enviable market share amid the majors. Over the last five years, NEM has achieved a growth of 22 percent year-on-year.

Export growth But the company’s ambitions are not just domestic. NEM has deep-tank fermenters of varying size, up to 10,000 litres of liquid culture. This provides good capacity to meet crop swings, says Barlow. There’s also a cost efficiency – with a selection of deep tanks there is less disruption caused by the downtime for sterilization, which is a cost. But it also opens an export opportunity, particularly to meet supply requests, without compounding supply to the local market. The Australian market commences in the autumn – March is typically the start of the supply for the cropping season with pulses having varying sowing windows, from March through to June.

Vetch treated with NEM inoculant. Crop is three weeks from germination and the image shows nitrogen nodules affixed to the roots of the vetch. Photo: NEM

In the relatively near market of New Zealand, NEM is already well established, supplying a majority of legume inoculants into the pasture market to seed companies. NEM already exports further afield, such as Europe and South America, but these trades can be exchange rate dependent.

“When we do business, we tend to do business with the leaders of related companies and key procurement and sales people,” explains Barlow, who adds they are looking to work with companies with a similar set-up to themselves, and particularly if it involves opening corridors to the Australian market. NEM also manufactures for companies in Australia and abroad.

It’s an ethos that has served the company well, gathering a 60-70 percent market share of the Australian inoculant business, which includes 80 percent of the peat inoculant business.

Absolutely faba-lous Barlow says the present time is an era of sustainability and regenerative farming practices, while noting rhizobia for agriculture systems has long since contributed to soil health and economic benefits. “The replacement of nitrogen fertilizer with biologically-fixed nitrogen is estimated to save Australian agriculture approximately AUS$4 billion per year,” according to the NSW Department of Primary Industries [Ref 1].

Pulses are part of the legume family. They play a large role in traditional cuisines throughout the world, but Zinga makes the point that a future driver for pulses is the growing demand for pulse-based meat.

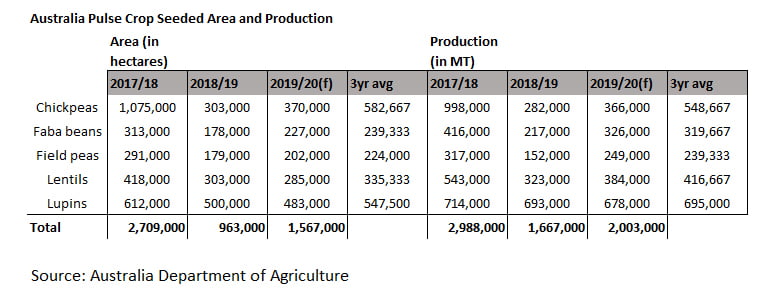

In Australia, winter pulse area is close to two million hectares (ha) based on a three-year average. The drought experience for 2018-19 years reduced long-term averages. Chickpeas and lupin are about 500,000 ha each, faba beans and field peas 240,000 ha, lentils another 330,000 ha and vetch around 200,000 ha. Australia’s five-year average pulse production up to 2017-18 was 2.1 million t (five-year average) [Ref 2].

Another key legume segment within Australia is summer legumes, encompassing a range of species with the key crops being mung bean, soybean, peanut and pigeon pea. Sown area fluctuates on summer rains. Mung beans range from 40,000-80,000 ha, while soybeans average 50,000 ha. The soybean area – and therefore the inoculant market for soybeans – is small compared with Brazil, a giant of soybean production, where around 82 percent of the 35 million ha of cultivated soybean surface already uses inoculants [Ref 3].

International price fluctuations can drive an increase in hectares. In 2017, the area for chickpeas in Australia swelled to one million ha because of a run-up in international prices, driven by Indian demand for supply which was then in the range AUD$1,000-$1,200/t.

Australia exported an average of 2.6 million t of pulses in 2015-2018, yielding $1.99 billion in revenue, with large customers being Bangladesh, Pakistan, Egypt and India, the largest with around 864,000 t. This is against a domestic use that is estimated at 500,000 t by AEGIC [Ref 2].

Long-term game When describing NEM’s future development, Barlow first takes a step back and reflects on the experience of his own farming family.

“For 150 years, we’ve gone to the casino.” The focus has been on the crops sown and then waiting for the rains, and in many ways the inputs have been discretionary, he elaborates.

But discretionary products are not what Barlow is aiming for as a business. What might be described as a strategic focus for new growth platforms NEM’s research draws on markets beyond its inoculants business. Barlow has been looking at key areas of R&D, highlighting where crops and environments have performed better. One of these areas relates to carbon capture, how agriculture systems will benefit from carbon sequestration credits through various practices and what could be done for farmers to register carbon credits for a new source of income.

“NEM’s other areas of focus are being assessed on targeted crops, including formulation performance and ideal application method, be it biological seed treatment, soil or foliar application to reduce the reliance on traditional chemical and fertilizer applications. These new solutions will provide an option in the growing area of regenerative systems.”

REFERENCES [Ref 1] www.dpi.nsw.gov.au/agriculture/soils/australianinoculants-research-group [Ref 2] AEGIC - Australian Export Grains Innovation Centre, using ABARES data [Ref 3] New Ag International – Soybean Inoculant Market March/ April 2020

Shanghai Fondin Bio-Tech Co., Ltd. was established in 2006, a high-technology enterprise specializing in new fertilizer R&D production and sales. The company is a leader in water-soluble fertilizer production in China. Chief Editor Luke Hutson speaks with Chen Wei, Shanghai Fondin Bio-Tech Co., Ltd., managing director.

Interview with Mr. Chen Wei, managing director of Shanghai Fondin Bio-Tech Co., Ltd.

What is and what is not a water-soluble fertilizer (WSF) in your company's definition? Fondin’s definition of the WSF is consistent with China national standards of macronutrients WSF (NY 1107-2010), such as N+P2O5+K2O ≥50%, TE between 0.2 percent to three percent, etc. But we take stricter standard for the insoluble content rate – the national standard is ≤five percent, and our standard is ≤0.1 percent. We conduct the same standard for our products sold in China and other countries. We don’t take the raw material fertilizers for fertigation or foliar spray into account, like industrial grade MKP, MAP.

What do you estimate as the approximate size (by volume) of the water-soluble market in China? It is really hard to get the exact statistics about the WSF market in China, but we think that the product of WSF is estimated to be about two million tonnes in the China market, mainly the macronutrient WSF powder products, and WSF with amino acid, or seaweed extract or humic acid not included in this figure.

How does Fondin break down the market by consumption, i.e. what percentage is greenhouse, horticulture, orchard, fields? Out-of-season greenhouse vegetables, especially in Shangdong province, is the first and the most important market of Fondin WSF products. At one time, the greenhouse vegetable growers in Shangdong province usually used the conventional compound fertilizer; but after they tried our products, they found our WSF worked more effective, with more yield and better quality. After greenhouse vegetables, we entered the fruit tree and horticulture markets as well. In recent years, the row crop market is becoming another focus of ours. Nowadays, the greenhouse vegetable market makes up a relatively significant share of 55 percent, fruit tree about 30 percent, horticulture 10 percent and row crops five percent.

Mr. Chen Wei, managing director of Shanghai Fondin Bio-Tech Co., Ltd.

What provinces in China are the largest consumers of WSF? Shangdong province is the largest consumer of WSF in China, especially for out-of-season greenhouse vegetables, followed by Yunnan and Guangdong provinces. Years ago, numerous fruit trees in Guangdong province were felled because of diseases. Hainan province, as the main producer of tropical fruits, is also an important consumer of WSF.

Please tell us about Fondin – how many production factories do you have? what WSF products do you make at them? We have only one factory, located in Lin-gang Special Area of the Shanghai Pilot Free Trade Zone of Shanghai city. The factory has two workshops: one is for manufacturing the powder products with an annual production capacity of 100,000 tonnes; and the other is for liquid fertilizers with an annual production capacity of 50,000 tonnes. We just launched the new powder product manufacturing system – this system operates at about 40 percent of the full capacity for the production of powder WSF. Delivery of the raw materials into the preparation tank, automatic pre-processing, accurate formulating, intelligent mixing and packaging and stacking, anti-counterfeiting system, precise environmental control – all these production processes integrate perfectly in the new system. The liquid products workshop is for the production of liquid WSF, like the products of mineral nutrients, seaweed extracts, amino acid or humic acid.

What volume do you produce each year? Right now, the annual production reaches nearly 40,000 tonnes, among which 85 percent are powder products, including WSF of macronutrients + TE, WSF of secondary nutrients, organic and inorganic WSF, WSF of micronutrients. In the powder products, the NPK compound fertilizer of (2:1:3) account for about 50 percent, (2:1:2) and (1:1:1) about 35 percent, and (3:1:1) and (1:4:1) about 15 percent.

The liquid products, mainly biostimulants including enzymatic hydrolyzed seaweed extracts and its derivation products, amino acid peptide and its derivation products, and humic acid and its derivation products, account for about 15 percent of the total production, and this proportion would continue increasing in the future.

What is driving the increase in consumption of WSF in China? From the customers side, the demand for high-quality vegetables, fruits and other crops is increasing, which promotes the increase of high-quality agri-inputs. Meanwhile, the expansion of protected farming and modern farms, and the planting of novel varieties of vegetable and fruit drive the increase of WSF in China.

What changes in demand have you seen as Fondin? The market of the novel fertilizer is changing now in China. At the national level, it is correct to reduce the use of pesticides and fertilizers. In past years, fertilizer was overused with lower efficiency to get higher yield. In the future, the demand for fertilizer would be on two tracks: one is to enhance fertilizer efficiency by innovation, to reduce the usage amount to a reasonable level; the other one is to increase the application of high-quality organic matter, to improve soil quality and the growing environment of the crops, which is also one of the focuses of Fondin in the coming years.

I notice some of your products include humic acid (HA). Which market are these products designed for? Yes, this kind of product is listed in our product portfolio. We found that in some greenhouses that have been planted for a long time, more and more fertilizer is required in the application, but more and more problems with crop growth, and higher and higher nutrients content in the soil. As a result, the crop output is affected. When humic acid products are applied in these greenhouses, the total usage of fertilizer is declining, but the crops perform better, with more yield and higher quality.

What annual growth rate do you estimate for WSF in China in previous five years and the next five years? According to our experience, the annual growth rate of the last five years was around 25 percent, and it will probably slow down in the next five years.

Do you have plans to launch a new WSF product in near future? We just invested in two new fully automatic production lines last year, which only need five workers to produce 200 tons of finished products in eight hours, with greatly improved production efficiency and lower costs. This is a remarkable innovation in the world. Our mission is to develop this factory to be the WSF manufacturing flagship in the Asia-Pacific region. In the future, we will build the new factory to further expand the production capacity. At the same time, biological products in agriculture is also our interest, and we believe these products would be the direction of WSF upgrading .