Photo: Kassiana Bonissoni – RuralPress

New AG International had first-hand access to the unprecedented study on the Brazilian fertilizer market for coffee plant nutrition. The survey, conducted by Spark Smarter Decisions, pointed out that this sector had a turnover of an impressive USD$966 million in the 2020-21 season. Leonardo Gottems writes.

A recent survey on Brazilian fertilizer usage on coffee nutrition shows that products for conventional NPK fertilization (with the primary macronutrients nitrogen, phosphorus and potassium) currently concentrate the largest share of the market, at 92 percent. The percentage represents sales of USD$888 million.

On the other hand, foliar fertilizers, composed of micronutrients, macronutrients or amino acids applied to the aerial part of plants, are equivalent to six percent of the total market. This meant $57 million of sales in the coffee fertilizer sector. Within this segment are the biostimulants, which include amino acids and protein hydrolysates, humic substances, micro-organisms and inocula, and algae extracts. Spark classified this group as "highly relevant in the foliar applications that were carried out in the crop in the 2020-21 season.” According to the survey, the average adoption rate recorded was 21 percent.

Products classified as soil correctors and conditioners correspond to the remaining two percent, or $21 million in sales. Correctives are used to balance the acidity, alkalinity and sodicity present in the soil while providing nutritional elements such as calcium and magnesium. In turn, soil conditioners contain nitrogen, calcium, phosphorus, potassium, magnesium, sulphur, boron, chlorine, copper, iron, manganese, molybdenum and zinc.

Demand According to Spark's project coordinator, Davi Caxias, in volume, the coffee growers demanded 4.3 million tons of fertilizers. Of these, 2.9 million tons were in the NPK segment, while 1.3 million tons were in correctives and soil conditioners and 12.5 thousand tons of foliar fertilizers.

Davi Caxias, Project Coordinator, Spark Smarter Decisions

"The adoption of treatments reached 100 percent of producers,” noted Caxias. “This is equivalent to saying that at least one nutritional management operation was carried out by the producers. The average investment by the coffee grower, indicated in the survey, was $473 per hectare (ha).”

Caxias points out that the level of investment by the producer is uneven, compared to the type of coffee grown. While for Arabica variety coffee the average investment reaches $496 per hectare, for robust variety the same indicator is $383 per hectare.

“The BIP Spark also shows a significant difference in terms of average investment, by region, in coffee nutrition. In the Cerrado Mineiro (Brazilian state of Minas Gerais), for example, figures confirm that the producer invests on average 26 percent more than in Zona da Mata (northeast region of Brazil)," noted Caxias.

Categories and brands As for the adoption rate of nutrition products, by category, the Spark study points out that NPK fertilizers lead the coffee grower's preference, with 99 percent. In sequence, there are foliar fertilizers (66 percent), correctives, and soil conditioners which add up to 39 percent.

"We detected the enormous potential for increasing investments in the nutritional management of coffee, especially in the foliar fertilizers segment," said Caxias. BIP Spark also pointed out that the 1,200 producers interviewed mentioned more than 170 companies and 1,000 commercial products. "Such data indicate a highly competitive and fierce market scenario.”

According to Caxias, the survey also investigated indicators of the grower's adhesion to specific products and companies operating in the sector, in addition to the knowledge of producers concerning manufacturers and commercial brands of fertilizers. For him, the lack of knowledge of the coffee grower about commercial brands and names of manufacturers, for example, is remarkably high given the relevance of the fertilizer sector as a whole. "There are, therefore, opportunities for companies to expand investments, aiming to gain customer loyalty and gain more access to the market," he noted.

The Spark research includes interviews in the states of Minas Gerais, Espírito Santo, São Paulo, Bahia, Rondônia and Paraná – the most relevant coffee producers in Brazil. The company confirms this first study is now part of an annual survey, the BIP Café (Business Intelligence Panel).

Potential and challenges "We are facing a robust, promising market. The movement close to $1 billion in the 2020-21 season demonstrates the strength of the technology and its weight in the production of Brazilian coffee,” said Caxias. “Another aspect to highlight in this scenario is that adherence to treatments reached 100 percent of the producers, which is to say that at least one nutritional management operation was carried out by the producers."

Caxias added that the survey detected "huge growth potential for increasing investments in the nutritional management of coffee, mainly in the foliar fertilizers segment. As this is the first study of its kind, we have not yet built a historical series that allows us to measure this trend more accurately. Certainly, in the next surveys of this

SINDIVEG-Plantacao-de-cafe Photo-CNA

kind, we will be able to provide more details regarding trends in handling and adherence to products and technologies in the segment. In general terms, we believe that it is worth reinforcing that the level of investment by the producer is uneven compared to the type of coffee grown."

The market scenario, according to the survey, shows a marked diversification of brands, products and manufacturers. The great challenge, the authors point out, is in the companies' ability to build solid commercial brands and/or highly credible corporate identity.

"There is a huge path to be taken by companies in the sector, even for companies that already enjoy a higher perception by the producer, to gain loyalty to commercial brands, products, and technologies," said Caxias.

The future: Nutrirrigation As well as advances in product research and development, there is an accelerated process of advancement in fertilizer and nutrient application technologies. For some time now, drip irrigation has been growing in Brazil, with water being carried by the crop through pipes over the land. Now, however, the use of these pipes for the transport and application of fertilizers is gaining strength – the so-called fertigation.

"Fertigation is a reality. The practice is indeed adopted. However, the survey found that adoption

Gabriela Terra, agronomic specialist, Netafim

indicators are not yet considered relatively low – we cannot detail such numbers," said Caxias.

In this scenario, a new concept emerged in Brazil: the so-called "nutrigation". Gabriela Terra, an agronomic specialist at Netafim, argues there is a difference: "Fertigation consists of the application of fertilizers via an irrigation system. While in conventional fertilization on coffee, the fertilizer is applied three to four times, fertigation allows for better parceling of this application, that is, the plant will have ‘food’ in a more divided way when compared to conventional fertilization, thus optimizing the farm's fertilization."

As for nutrigation, Terra point out that it is "fertigation in an improved way, where it is possible to divide it in an adequate way to the

phenological stages of the plant. The system has fertikit and stock solution boxes that are prepared according to the fertilization plan of each farm, and it is possible to carry out fertigation throughout the irrigation, without the need for a person to mix and inject as in fertigation."

The importance of this technique is even greater for the coffee culture, which is highly valued for its beverage quality and sieve classification.

"With this, nutrigation helps in the production of coffee with higher sieves and superior drink quality, as it allows fertilization to be carried out following the phenological stages,” said Terra. “For example, in the grain filling phase, the demand for N and K and some micronutrients can be higher when compared to other

phases. This technique is recommended for producers who aim to increase their productivity and have an excellent product.” ●

Products and Trends NEWS

By Rick Melnick, Vice President, Global Business, DunhamTrimmer, LLC

There is a lot to like about pheromones. One might say they represent the quintessence of sustainable crop protection: they are natural (or naturally derived) compounds that are highly effective in controlling pests, yet have a non-toxic mode of action with no adverse effect on non-targets or the environment and maintains biodiversity. What's not to like?

A grower might answer quickly: the cost. Pheromones are notoriously expensive to manufacture and until now, widespread adoption has been consequently limited to production of high-value crops. There are indicators that all of that is about to change, however. Rather quickly.

Slow development, historically Pheromones are a part of a broader group of substances known as semiochemicals, from the Greek semeon (a signal). Pheromones are chemicals released by one member of a species to elicit a specific interaction with another member of the same species. These signals may relate to alarm, aggregation, or mating.

Insect chemical communication was first observed by the French entomologist Jean-Henri Fabre. In 1879, Fabre had placed a female peacock moth in a wire-gauze jar, for study. By evening, his house had become infested with male moths. Despite the revelation and subsequent research, it would take almost 100 years before the chemical structures of major agricultural insect pest sex pheromones could be described and synthesized.

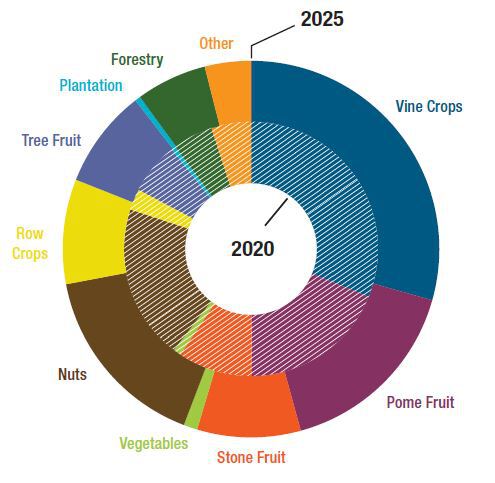

Since pheromones companies commercializing lures for pest monitoring began to emerge in the 1970s, it has taken another 50 years for the pheromones industry to achieve its modest level of development. The biologicals market analyst firm DunhamTrimmer estimates 2020 global pheromone active ingredient sales at ex-works USD $388 Mn. Most of that growth has come over the last 20 years, as mating disruption has supplanted lures and monitoring as the primary use for pheromones. Currently, Europe has the highest percentage of the treated hectares (33 percent), slightly more than in the U.S.

Source: 2021 DunhamTrimmer Global Pheromones Market Report

Resistance and residue management have been the main drivers behind this growth, not to mention an evolving legislative environment and consumer demands that encourage the use of low-impact products. But while these drivers affect the entirety of agriculture, the high cost of synthesizing pheromones has limited their use to the highest value crops. DunhamTrimmer estimates that in 2020, 88 percent of global pheromone use took place in vines, tree fruit and nuts. Conversely, only

three percent took place in row crops, mainly cotton and rice. Disruptive manufacturing technology High cost of manufacturing has meant a high cost of goods sold (COGS) for pheromones, translating to high cost per hectare treated for growers. But new innovations in pheromone synthesis over the recent past promises to reduce pheromone COGS substantially. This development brings with it the possibility of rapid expansion of pheromones into broadacre crops, in particular corn and soybeans.

At the heart of these innovations is the advent of synthetic biology: use of genetically-engineered microorganisms such as bacteria, yeasts and micro algae to manufacture valuable metabolites. In essence, these microbes can be reprogrammed to manufacture pheromone actives. Since the microbes are genetically engineered, but are never released into the environment, the process is deemed an acceptable form of manufacturing. The pheromone metabolites are deemed "nature identical."

Opportunities stemming from the convergence of these drivers appear to be substantial. As a result, the pheromones market has attracted the interest of numerous outside investors looking to capitalize. From 2018 to 2021, investments totaling more than $290 million have been made in pheromone companies – equivalent to 82 percent of the current market’s value. This influx of capital promises to drive further growth with a significant upside. ●

For more information on the 2021 DunhamTrimmer Global Pheromones Market Report, visit DunhamTrimmer.

For some time now, drip irrigation has been growing in Brazil, with water being carried by the crop through pipes over the land.

Mating Disruption $340.91 MnIMassTrapping/Lure & Kill $47.68 MnITotal Market $388.59 Mn

*Active Ingredient Sales, Ex-Work (Manufacturer) Base.

Disruptive changes in COGS means that pheromones sales into row crops are forecast to triple by 2025.