AUSTRALIA

Food is an abundant commodity in Australia and the food export industry is worth USD$34 billion, since the country exports 65 percent of all food produced. And the sector is not slowing down, as agricultural businesses grew five percent over the last two years, numbering 89,400. The gross value of Australian agriculture also rose by three percent to $46 billion in 2018-19, despite drought conditions. The sector is indeed recovering after several years of hardship on a farm level. Global agribusiness banking specialist Rabobank stated that 2021 will be a profitable year for Australian agriculture. This is underpinned by high commodity prices, positive seasonal conditions and low interest rates, and despite expected continuing trade tensions with China. Rabobank’s head of food and agribusiness research, Tim Hunt, said despite the turbulent environment facing the world as 2021 gets underway, global demand for food and agribusiness products remained “surprisingly firm,” while weather patterns were also favouring Australia ahead of competitors when it comes to production.

“And while foodservice channels remain compromised in many markets due to COVID-19 lockdowns and restrictions, the otherwise strong demand for food and agricultural commodities is seeing global prices supported – which is good news for Australian farmers,” says Hunt. He notes one key area for Australian agriculture going forward would be adjusting to a market more focused on environmental sustainability. “COVID-19 took the headlines from climate in 2020, but it didn’t alter the commitment of key players throughout the food and agriculture supply chain to mitigate climate change, prepare for its risk and find mechanisms to reduce and or recoup the costs of adjustment. “If the pandemic wanes in late 2021 as hoped, this quest will again rise to the fore, creating both opportunities and challenges. And it may prove to be the greatest of all the transitions facing the sector,” says Hunt. Demand for quality, safe horticultural produce in key markets is set to remain strong in a country already conscious of chemical use on food crops. The affluence of the economy means the population is at the forefront of food trends and echoes the move towards healthier food, with a lower environmental impact, as demanded in many European countries. Consumers are increasingly demanding food that has not been exposed to chemical treatments. The organic food sector is valued at $2 billion with an average industry growth rate of 13 percent over the last five years. The country also boasts the largest area of land under organic production in the world. As cleaner and greener food is heralded as the way of the farming future, it is creating a robust market for farming practices and inputs that work with nature, rather than against it.

Mineral fertilizer consumption plateaus The adoption of regenerative farming practices in Australia is gaining momentum among grain and fruit farmers alike. With an emphasis on soil health, microbes and beneficial insects, farmers are finding their reliance on harsh chemicals and synthetic fertilizers is waning. This also goes hand in hand with precision agriculture practices where blanket fertilizer treatments are no longer applied, but rather site specific and in meticulously measured quantities. The Australian Bureau of Statistics reports that synthetic fertilizers far outweigh organic fertilizers with ammonium phosphates the most widely used fertilizer by area in 2016-17. However, the area to which it was applied decreased by eight percent to 13 million hectares and the tonnes applied decreased by 14 percent to 963,000 tonnes. Urea continued to be the most applied fertilizer in 2016-17, both by the amount applied and the number of businesses using it. While the area on which urea was applied decreased five percent to 11 million hectares, the amount applied was virtually unchanged from 2015-16 at 1.4 million tonnes. Nationally, 21,800 agricultural businesses applied urea in 2016-17, a two percent decrease from 2015-16. According to a report by Ibis World, the market size of the fertilizer manufacturing industry is expected to increase with 11.6 percent in 2021. The primary negative factors affecting this industry are high imports and high competition. And since fertilizer prices tend to be set globally, changes in the value of the Australian dollar can significantly affect industry revenue. The anticipated weaker Australian dollar means Australian fertilizer products will be more competitive in overseas markets during 2021, providing an opportunity for the industry to expand by boosting exports. The market for liquid fertilizers is expanding and is expected to reach a value of $646 million by the end of 2024, signalling a growth rate of 3.7 percent since 2017. Investments by some of the country’s largest fertilizer manufacturers is not only improving research and development (R&D) of products, but distribution as well. This includes Incitec Pivot Fertilisers’ new fertilizer distribution facility at Port Adelaide worth $25 million, and Yara Australia’s expansion of its Boundary Bend Plant in Victoria. R&D is also being focused on formulating liquid fertilizers that could work as a combination of fertilizers and pesticides in order to reduce the overall chemical burden on soil for broadacre and home garden applications. Mineral liquid fertilizers make up 97 percent of the market and is projected to continue dominating the fertilizer space. The organic segment is anticipated to reach $34 million by the end of 2024. Australia’s liquid fertilizers market is segmented on the basis of mode of applications into starter solutions, foliar application, fertigation, injection into soil and aerial applications. Foliar fertilizers occupied the largest market share at 52 percent and is anticipated to reach $314 million by the end of 2024.

Shifts towards reduced fertilizer usage are being felt in the industry as alternative agricultural practices like regenerative agriculture is expected to slow down the growth rate of mineral fertilizers. Coupled with strong regulations of usage and trade of various fertilizer components, the market for organic materials looks promising. Biostimulants hindered by lack of regulation Worldwide agriculture is increasingly moving toward the use of biostimulants due to their ability to enable plants to better tolerate stress from changing environmental factors. These stressors include temperature rise and lower moisture levels caused by the effects of climate change. Since Australian farmers have particularly been put through their paces on the weather front, biostimulants present an exciting area of growth in agricultural inputs down under. Globally, growth is also being driven by mounting demand for organic agricultural products as opposed to food grown using chemical-based fertilizers and non-natural soil enhancements. Australia’s consumers are no different, and crops grown using biological inputs have ample room for growth. Availability and uptake of biostimulants is, however, still in its early stages. The country has a wide variety of formulations, classified in four major groups: humic substances, hormone containing products, amino acid containing products and plant growth promoting rhizobacteria (PGPR). But much market development is still needed to get a broad acceptance of the benefits of using biostimulants. Geoffrey Craggs, research analyst at the Northern Australia Land Care Research Programme, states European farmers employing biostimulants as a fundamental component in their farm’s management practices are reporting higher levels in soil fertility and increased crop yields in cereals and oilseeds. “By using naturally derived biostimulants, farmers are also reducing their reliance on costly traditional synthetic chemical-based fertilizers that, over time and through consistent application, can result in lower fertility from a build-up of chemical residues in the soil,” says Craggs. “Many varieties of ornamental crops, vegetables and fruits are benefiting from increased tolerance to, and recovery from, physical stresses, nutrient assimilation and quality improvements such as sugar content and colour, as a result of biostimulant use.” He notes that while the European Union (EU) has the largest share in R&D and use of biostimulants, he claims projections indicate Asia-Pacific will be the fastest growing biostimulant market by 2022. “There is a rising awareness and preference towards biostimulants in Australia, China and India as farmers are adopting contemporary farming and agricultural practices that feature the use of organic substances, in combination with sustainable farming methods. This will be strengthened by a rising awareness and preference toward biostimulants in these major agricultural economies.”

The industry, however, faces a number of hurdles in growing market share. Craggs says while the evidence in favour of biostimulants is strengthening, government action to generate policies that will enable formal regulatory compliance with defined standards criteria has been mixed. “Action in the Asia-Pacific region has been limited. In comparison, the EU has developed robust organizations such as the European Biostimulants Industry Council and, in the U.S., the Biostimulant Coalition, who are working to advance a definition of biostimulants for inclusion in a future piece of legislation. These and similar agencies are also engaging in scientific dialogue to identify environmental considerations and the safe use of products to be integrated into crop management programmes. “By contrast, little has been done in Australia to create and empower a suitable regulatory authority,” adds Craggs. “Consequently, without a framework responsible for regulating scientific trials and testing, the identification and assessment of risks and the enforcement of responsible marketing, Australian primary producers and consumers are at risk.” Concerns have also been noted regarding the quality of products sold in Australia, which supposedly varies widely, particularly when live organisms are involved. Further constraints include labelling that is often inadequate or generic, and products that are not always tested under Australian conditions. These present opportunities for companies producing quality products that have been tested and proven to work locally.

Biocontrol is growing Integrated pest management (IPM) is growing rapidly in Australia and is paving the way for increased use of biological control methods. The aim of IPM is to maximize the use of biological control while other control measures, especially chemicals, play a supportive rather than disruptive role.

Much work is being done on products that can be used in conjunction with each other. Lena Adam, vice-president of global strategic marketing fungicides at BASF’s Agricultural Solutions division, said much potential lies in the complementary use of biologicals together with conventional solutions. “The future for biologicals looks promising and a good balance of conventional and biological technologies will help farmers to produce enough healthy food to feed a growing population while addressing societal expectations and consumer needs,” says Adam. “The COVID-19 pandemic we are living through is also accelerating sustainability and health trends that started some years ago. The demand for healthy and fresh food will grow faster, and consumers will increasingly value more natural products.”

She notes the growing potential for biocontrol in row crops. “At the moment, only a minor percentage of the total biological market is found in row crops. But we see much opportunity for biocontrol not only as a seed treatment, which is widely used today, but also as a soil and foliar application.” Locally occurring natural enemies have become a key component to IPM programs and is recognized as a viable alternative to regular broad-spectrum insecticide programs in a range of horticultural crops. Most notably this includes citrus, strawberries, macadamia nuts and greenhouse vegetables. These beneficial insects consist of predators that feed on harmful insects and parasitoids which deposit an egg into the pest, usually at a critical life stage. The larva that hatches ultimately consumes and kills the pest. Having spent over 40 years working in the beneficial insects industry, Dan Papacek, director at Bugs for Bugs in Australia, says biological control of pests is on the cusp of becoming a mainstream practice in Australia.

“We are seeing much greater uptake due to various factors. Farmers have a greater awareness of alternative pest control, and pressure from consumers (including export markets) to lower maximum residue levels for many pesticides is pushing farmers to find alternatives. The use of chemicals is becoming regulated and not as easy to apply as it used to be. Anything that makes it harder to spray a poison will swing the balance in favour of alternatives,” says Papacek. “We have also seen system failure on a larger scale. We are regularly approached by growers who have been spraying increasingly more for increasingly less results. They often call us in desperation. All too often the pesticides themselves are inducing the problem.” Papacek maintains there are also problems with resistance in the standard approach. “Insects can be very quick to re-organize their genetic makeup to tolerate applied chemicals which in time leads to system failure.” Papacek notes while farmer’s attitudes towards incorporating biocontrol methods are positive, most growers are cautious about taking the plunge. “But if we can help them achieve equivalent, or better, results with biocontrol (as part of an IPM package) then they are enthusiastic.” The industry still has its challenges, and since biological control does not have a solution for every problem, Papacek believes chemicals will continue to play an important role. “Modern chemicals are generally less indiscriminate in their action and this is a good thing. It also means that it is easier to integrate the use of our delicate biocontrol agents,” he says. “Another obstacle to overcome is that supermarkets (which represent the buying public) still place great emphasis on the appearance of fruit and vegetables and therefore don’t really encourage IPM. While the only information to the consumer remains a visual cue, they will continue to select for the prettiest produce and this will put pressure on growers to spray to achieve the ‘perfect plastic product.’ Most fresh fruit and vegetables in Australia are still largely unidentified so the grower gets no reward for doing the right thing.” Precision agriculture Precision agriculture (PA) is gaining momentum as growers are looking to reduce input costs by optimizing technology and applying agronomic practices that target applications for site specific management. The adoption of PA varies among different crops, with cereal farming achieving the highest rate of adoption at 80 percent. In a survey of Australian grain growers conducted to gauge grower attitudes to crop and soil sensing and their role in nitrogen fertilizer management, Rob Bramley, senior principal research scientist in precision agriculture at the Commonwealth Scientific and Industrial Research Organisation (CSIRO) in Australia, found that whereas Australian grain growers have readily adopted machine guidance and autosteer, and a majority have access to yield monitoring, the rate of use of many crop and soil sensors remains comparatively low. “If we are to increase the use of PA, the results make clear that a greater effort needs to be made to increase the adoption of yield maps. This would be valuable as a lever to gain ‘buy-in’ from growers to sensing and PA more broadly,” says Bramley. “This is especially since we found that access to yield maps was significantly associated with the use of remotely sensed imagery, high resolution soil surveys, soil moisture sensing, digital elevation models (DEM), and variable rate application of fertilizers and soil amendments.” Over 40 percent of all survey respondents have accessed remotely sensed imagery of their farms, with 88 percent of users sourcing this from satellite-based platforms. Of the growers who have accessed remotely sensed imagery, 56 percent used it to guide variable fertilizer management and around 13 percent used it to guide crop choice or seeding rate. While 57 percent of respondents had the capacity to implement variable rate fertilization, only 52 percent actually did so.

Bramley says one of the biggest challenges in increasing the implementation of PA was access to good data analysis. “Farmers are busy for most hours of the day, and unless they employ people to manage the core functions of the farm, there is little time to properly analyze data. Furthermore, the expertise, availability and affordability of consultants who can is an impediment to greater implementation.” Vegetable growers are somewhat ahead in their views of PA. This was highlighted in Hort Innovation’s study into the level of adoption, which found that crop sensing imagery, yield forecasting from remotely sensed crop imagery, yield and profit/loss mapping, a range of soil mapping technologies, variable rate application, precision drainage technologies, and various drone applications are widely used. The purpose of the study was also to further introduce farmers to the different technologies and encourage greater adoption. In discussing concerns farmers had regarding the technologies, they found particular issues with regards to vegetable production needed to be targeted. This included variable rate applications for salinity, soil pH and nutrients, to achieve improvements in crop growth, water infiltration, crop uniformity and optimal placement of crop inputs. Cost was repeatedly mentioned as a key barrier by growers to commence adoption of PA technologies and approaches. The integration and compatibility of different technologies and sensors was also highlighted as being problematic. They also called for better systems to integrate service provider-collected data and self-collected data. Overall, farmers stated the need to simplify all aspects of PA implementation to minimize steps for growers to obtain, access and interpret data. As a modern agricultural country, Australia has seen a decent amount of farmers implementing technologies and solutions that are lighter on the environment and poised towards better sustainability. And while most of these solutions are not new to the country, finer details to encourage greater adoption still need to be ironed out.

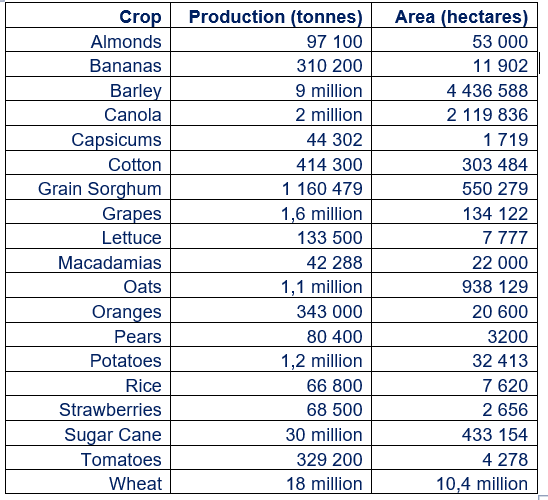

Source: Australia Bureau of Statistics

Figure 1. Main crops produced in Australia 2018-19

Photographs: Page 1: Macadamia nuts By Barmalini Page 3: Macadamia nut tree orchard/Glass House Mountains, Australia By Martin Valigurske Page 6: Australian Vineyard By Ben Goode Page 8: Sugar cane harvest in Queensland, Australia By Johan Larson