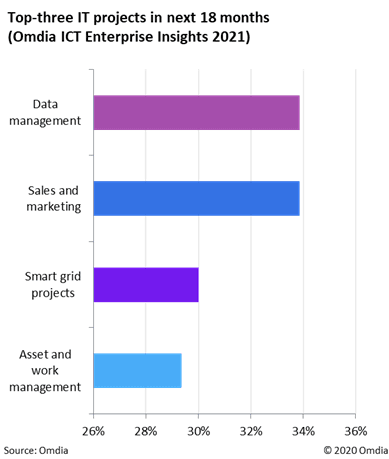

Utilities face greater challenges than ever before—especially in the wake of COVID-19 where public budgets are restricted, and rate increases are likely to be opposed by public pressure groups. The real issue is that utilities can’t wait for the right time to invest in digitalization, with the need for technology adoption an existential challenge for them. IoT is here to help utilities (another 183 million smart meters will ship worldwide in 2021 alone), but they are not data management experts and need the support of cloud services, analytics, and the supply chain.

SaaS and cloud hosting haven’t typically played well against utility concerns: it creates Opex spend that can’t be applied to new rate cases in the same way as before, and raises cybersecurity concerns—which is still rated the number one challenge by utilities for digital projects. However, this is no longer enough to prevent utilities taking the plunge, and adoption is accelerating. The number of smart meters for which utilities pay an annual cloud-hosted software fee will exceed 100 million for the first time in 2021, based on North America and Europe alone.

In fact, over 50% of utilities surveyed by Omdia say they're already trialling or fully deploying SaaS in some part of their business. The same proportion also say their budgets for enterprise-wide data management is increasing in the next 18 months, despite the challenges from COVID-19.

Utilities may typically be slow drifting, but cloud adoption will reign in 2021 if they are to maximise the power of their data.

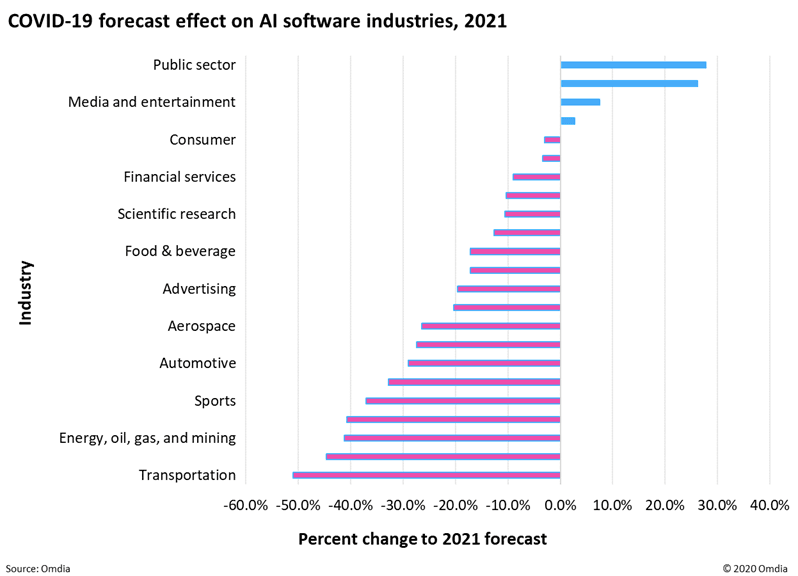

In the immediate term and over the forecast period, there will be an acceleration in AI adoption in the healthcare industry owing largely to COVID-19. Omdia expects that COVID-19 will drive a significant revenue growth in 2021 for the healthcare AI software market and has upgraded the year-over-year growth forecast to 84.0%. This represents a change of 26.1% YoY from pre-COVID-19 projections (the second-most positive forecast change to an AI software industry in 2021).

The COVID-19 pandemic has accelerated the development of AI software in the healthcare sector and has led to further targeted investments in AI-based drug and vaccine research, medical imaging, and machine learning tools for patient screening, triage, and monitoring.

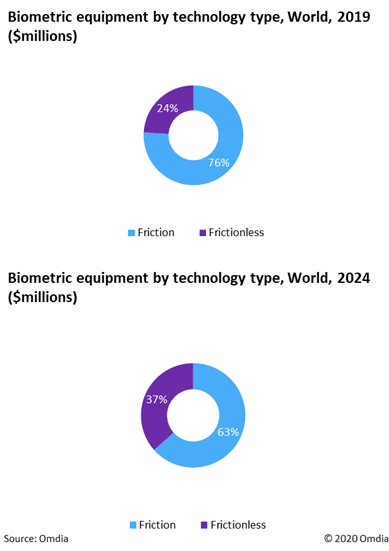

Facial recognition and frictionless fingerprint readers will fuel the growth of biometric technologies in access control systems COVID-19 has undoubtedly caused lasting change to industry, but may yet accelerate technology adoption in 2021; from rising early adoption of smart building applications (e.g., for sanitation), wireless connectivity for retrofit projects, and new frictionless hardware. Frictionless biometric readers can scan and process biometric data without requiring the user to initiate physical contact with the device. Nearly every facial recognition reader, most iris recognition readers, and a newly emerging class of frictionless fingerprint readers installed in access control systems today are defined as frictionless biometric modalities. Growth in the use of facial recognition readers will be supported by improved 3D facial recognition AI and advanced algorithms in access control software. These algorithms are capable of successfully identifying individuals based on more discrete features and expressions that can be detected even when lighting conditions change and when an entrant’s facial features are partially obscured. The COVID-19 pandemic is expected to accelerate a transition to frictionless biometrics as end users will seek to invest in hygienic alternatives to readers that require physical interaction with surfaces that could act as vectors for viruses. Omdia projects that the market for frictionless biometric readers will grow over 15% in 2021, while demand for friction readers will grow less than 5% that year.

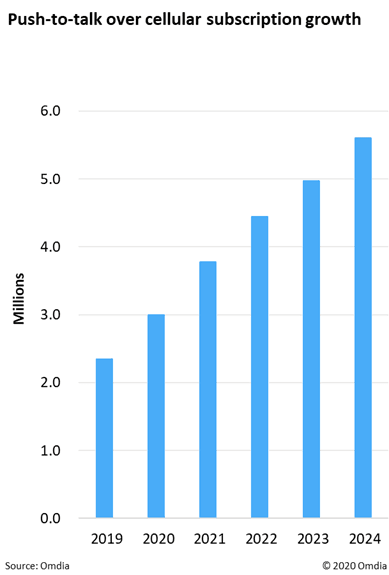

Mobile network operators emerge as key partners for public safety mission-critical networks The model for national mission-critical LTE networks has been in gestation since the US battle for the D-Block culminated in establishing the FirstNet Authority in 2012. Efforts in the UK, Korea, and the UAE embraced a diverse set of approaches with varying degrees of government network ownership. In 2021, paths are converging upon public/private partnership models, as exemplified by the US government's 2017 contract with AT&T, the UK's contract with EE, and Finland's deal with Elisa. Subsequent national decisions will leverage the mobile network operator's geographic coverage advantage and 3GPP mission-critical feature specification to cost-effectively deliver services. As nations gain confidence in the public/private model, the adoption trend of national public safety broadband networks will significantly accelerate. By 2024, Omdia projects 5.6 million push-to-talk over cellular subscriptions will be in place. By converging voice/data operations on a single device, law enforcement, and emergency medical services will dramatically expand access to cloud-based applications for increased operational efficiency. Beyond access to cloud applications, the shift to mission-critical LTE networks for public safety enables broader access to mobile video applications. Flowing video from vehicles and body-worn cameras to control rooms helps boost situational awareness for incident commanders. Likewise, the growing use of drone platforms for video transmission will drive further mission-critical data growth.

In 2020 the IoT topics in focus were 5G and edge computing. In 2021, expect to see the idea of software defined automation begin to be added. For decades, the industrial sector has battled with connecting products from multiple vendors, which often utilised different (and proprietary) protocols, interfaces, and data formats, resulting in significant integration challenges and costs for end-users and often resulting in vendor lock-in. At the same time automation vendors have struggled with a mature market ($217 billion in 2019) with growth estimated at 1.1% (CAGR 2018-23).

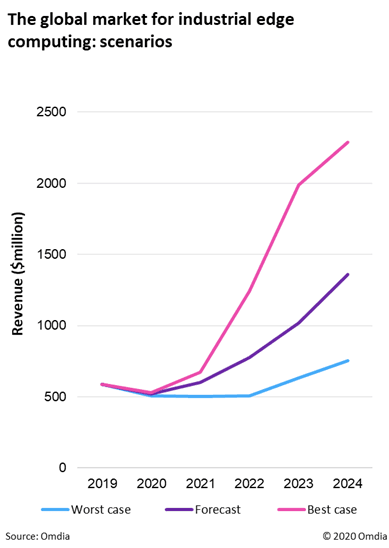

This landscape is changing, both with the entrance of new vendors and approaches from the Enterprise IT sector, as well as the shift in focus from hardware to software from many of the leading OT vendors. Already a well-established and growing trend is for Industrial PCs (IPCs) to integrate additional capabilities, such as motion control and machine vision through software. However, alongside this, end-users are increasingly looking to access additional analytics close to the source (in partnership with, or instead of using the cloud), driving rapid growth in industrial edge computing devices. This market is forecast to reach $4.8 billion by 2030. As well as the integration of additional compute power, new software platforms that can leverage new solutions such as containers and VMs (virtual machines) are facilitating the decoupling of automation hardware and software. What does this mean for manufacturers? Beyond removing vendor lock-in, accelerating innovation and reducing cost, this will bring a transformational impact on how automation is delivered. In the same way that the mobile phone’s move to a multi-function device supporting a range of applications, edge compute and software defined automation will drive hardware convergence in industry. This will shift focus from hardware capabilities (and limitations) to applications running across multiple application on increasingly application agnostic devices.