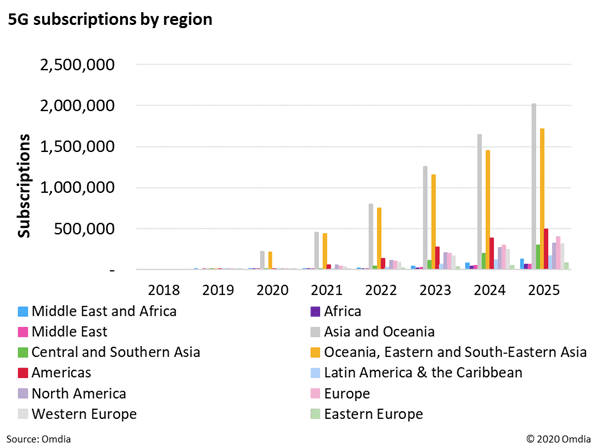

2021 will mark a second wave of acceleration of 5G deployments for service providers Globally, 5G will reach 553 million subscriptions in 2021. Its distribution across the globe will be more balanced as the US and Europe will leverage the introduction of Apple's 5G devices. With markets approaching critical mass, the deployment of wide-ranging and denser 5G coverage will also facilitate the commercial adoption of 5G in B2B and B2B2x markets—these have so far, have been limited to testbeds small and large trials.

Some 5G SA deployments and some 5G-riven MEC have already happened in 2020, but the bulk of the market will be ignited in 2021. With that, network slicing will break out of the trial-stage and start gearing up to commercial reality. Affordable 5G devices are on the horizon. Service providers are advocating for sub-$300 5G devices, but emerging-market affordability is still some time off, and 5G will remain mainly a rich-economy affair for most of 2021. Ecosystem management remains the "killer app" for service providers. 2021 will provide evidence that those CSPs that have invested in partner-orchestration capabilities are the real beneficiary of a technology that would otherwise be just another G in the connectivity roadmap.

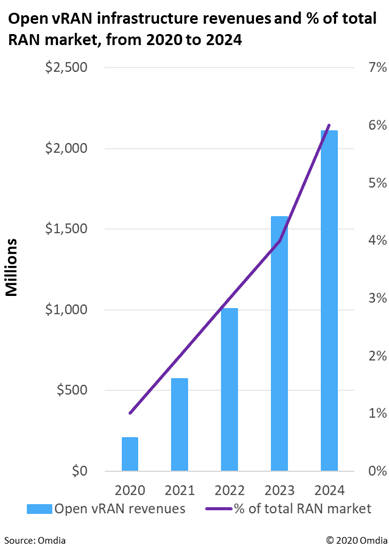

Operator adoption of Open virtual RAN (vRAN) accelerates

Dish networks will start deploying its new mobile network in 2021, giving Open vRAN proponents a second large-scale greenfield proof point for their solutions. Operators will be expanding trial and proof of concept (POCs) for testing Open RAN solutions, with deployments now approaching 1,000 sites in 2021—a major expansion from earlier trials of a dozen or more sites, signalling growing open vRAN maturity.

We expect to see greater message differentiation between solutions for rural coverage-driven networks and those built for high-capacity networks.

Radio vendors will focus on not only low-cost units but also high-performance ones to support massive MIMO. Meanwhile, solution integration will be a major focus of suppliers.

How incumbent vendors deal with this trend in 2021 will be key to watch. Does Nokia and Samsung become more aggressive in their support of Open vRAN and announce operator contracts? Does Ericsson announce its Open vRAN solutions? Does Huawei warm up to this? All of these are indicators of operators’ levels of interest in Open vRAN.

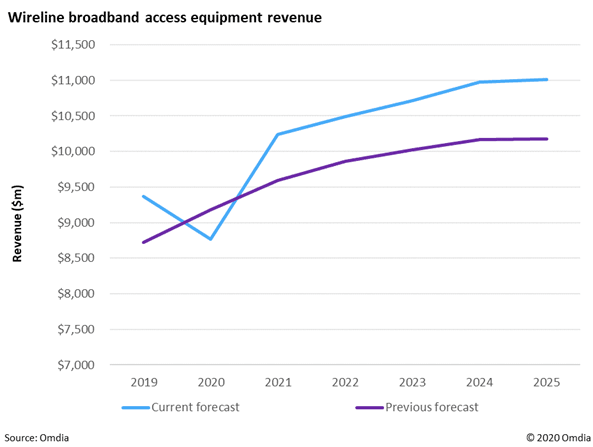

Broadband access networks will remain vital for global connectivity in 2021 Overall, the broadband access equipment market continues to grow, further propelled by demand generated by the pandemic and more people working and learning from home. This demand will continue in 2021 due to renewed lockdowns and quarantines until a vaccine becomes widely available. Operators cooperating with Clean Network policies established by the US State Department are awarding significant contracts to non-Chinese network vendors. Smaller vendors with a small share of the Europe and parts of Asia are picking up contracts previously won by Chinese vendors. These policies and activities will likely continue in 2021. COVID-19 related network demand has accelerated the movement of operators to 10G networks. Virtualization will be a major driver in 2021 as operators seek efficient and automated networks. Cable operators continue to shrink their head ends and distribute functions into the outside plant but will resume centralized upgrades and node splits to fulfil immediate bandwidth demands in the short-term. Integrated operators are looking to adopt fiber access to support multiple service segments, including access, transport, and campuses. Revenue opportunities related to the use of 10G PON for non-residential services continues to gain traction into 2021.

Wireline broadband access equipment revenue

Automating the increasingly complex network and service management environment has become a major priority for service providers The COVID-19 crisis has impacted service provider spending plans, but technology never sleeps, and several key areas of telecom IT will demand attention in 2021. Overall telecom IT vendor revenue is expected to grow by 2.3% in 2021, a welcome improvement on this year’s anticipated 0.6% decline, although still below the 4% CAGR for the period to 2025. However, despite the overall sluggishness there will be strong areas of growth, especially around anything to do with AI-driven network automation, data management, and monetization. Automating the increasingly complex network and service management environment has become a major priority for CSPs, along with the AI and data management capabilities required to support this. Service providers also need to invest in customer engagement solutions to digitize and unify the customer experience and the 5G monetization tools required to support a wide range of new services and business models. Moreover, underlying it all is the continuing shift to the cloud and the need to adopt cloud-native technologies and practices.

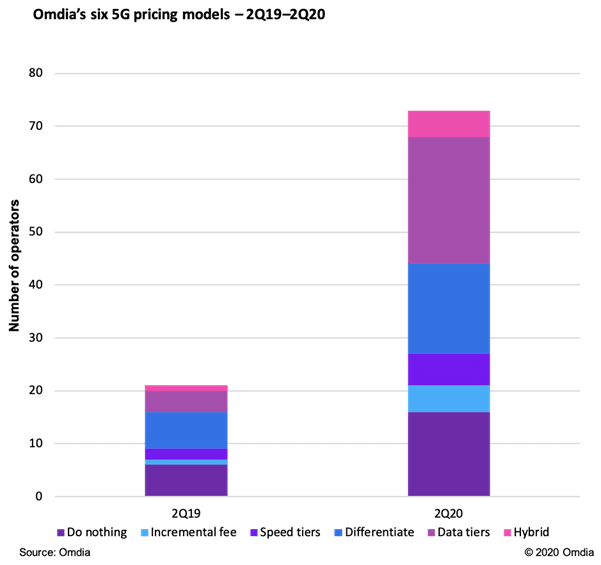

Pricing to “differentiate” entices the consumer to upsell to 5G How to monetize 5G for consumers will continue to be the biggest challenge for operators in 2021. As of 2Q20, 77% of 5G operators did not bundle 5G-rich apps. Conversely, 23% or 17 of the 73 5G telcos tracked, did have a differentiated pricing model and bundled at least one 5G-rich service in 2Q20. This compares to just seven “differentiate” pricing models in 2Q19. Of those that didn’t bundle, 33% simply offered data tiers, with or without non-5G ready content, such as traditional OTT services (e.g., Spotify). A further 22% did not launch any new plans for 5G—a “do nothing” strategy—opening only existing plans to next-generation users. We are still waiting for operators in numerous developed countries to even roll out their first 5G-rich app. The COVID-19 pandemic’s resulting economic and job uncertainty is not going away any time soon. However, bundling a 5G-rich app (e.g., 3D AR shopping, e-books, or VR cloud gaming) alongside more expensive 5G plans, will make consumer upselling easier for telcos. In turn, this can lead to mobile ARPU growth/stability, lower churn, and incremental revenue as consumers buy more expensive 5G plans and a 5G handset.