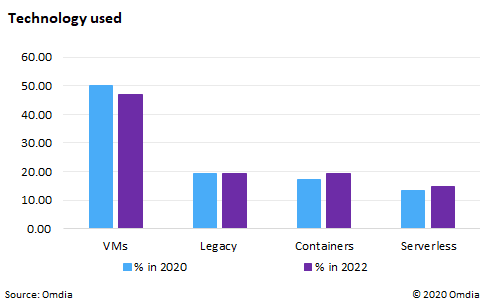

The move to adoption of cloud-native for production workloads in enterprise customers, is at the expense of VMs

China expects to move from more than 52% VM-based applications today to just over 48% in 2022, with legacy workloads dropping from 19% to just over 17% in the same period. While, globally, legacy applications remain flat at 19.3%, in LATAM legacy is set to increase by 0.5% between 2020 and 2022. Healthcare and retail demonstrates a preference for container technologies over serverless. Between 2020 and 2022 containers use is predicted to grow almost four times that of serverless. Government shows a preference for serverless with its use increasing 2.4% between 2020 and 2022, compared to 2.3% for containers, with most workloads moving from VMs, although a small, 0.8%, decline in legacy is expected over this time period. SMB (revenues less than $499 million) showed moderate increase in cloud-native use at the expense of VMs, a swing of 3.4%. This was similar to large organizations (greater than $20 billion in revenue), the difference being large organizations use of cloud-native was more advanced representing 36.3% by 2022 compared to 33.5% in SMB.

All of this means that organizations must look to adopt new approaches to manage this hybrid environment, as it changes from an infrastructure-centric to an application-centric environment.

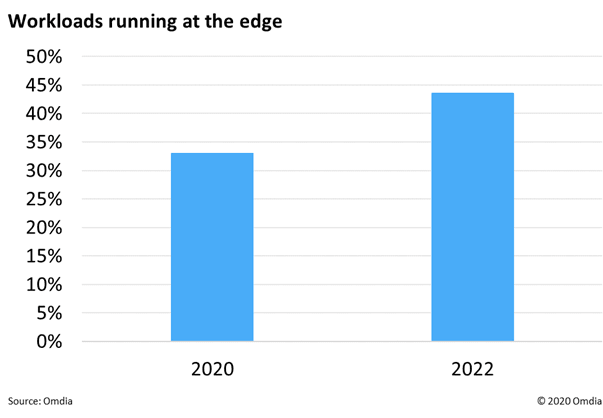

With no standard architecture for edge computing hardware and software, the market will be driven by use-case demand in key segments such as manufacturing and retail 11.9 million DC servers were shipped in 2019, of these 2.4 million were deployed at the edge, and by 2021 Omdia forecasts this to be 3.2 million or 22.5% of the total servers shipped. Omdia expects the market for edge deployed servers to continue to grow out beyond 2021 to enable low latency and secure processing of large volumes of data. As the count of IoT connected devices grows, enterprises increasingly adopt new software applications (such as AI) to aid employees in certain tasks, and the nature of devices and applications changes, with the collection and real-time processing of data become increasingly important. The growth of open compute servers at the edge is a consequence of telcos and CSPs expanding their service offerings by placing compute closer to their customers.

A large portion of the servers which telcos have deployed at the edge so far are used for content delivery networks (CDNs). The growth is driven by telcos pursuing new revenue streams such as video content delivery, vehicular communication for autonomous vehicles, AR/VR, and gaming.

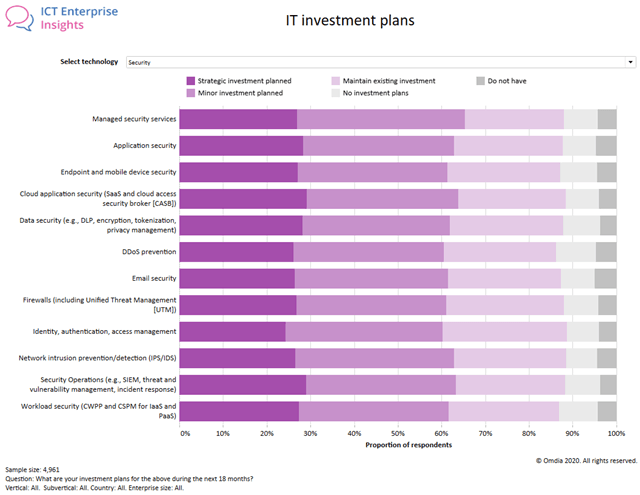

Shift to cloud dominates infrastructure security trends The effects of the pandemic have seen plenty of evidence of the planned moves to cloud-based security being significantly accelerated. Omdia’s ICT Enterprise Insights show that both cloud application security and cloud workload security are a focus for strategic investment for security in the next 18 months (29.1% and 27.4% of survey respondents respectively), alongside planned strategic investment in security operations (29.0% of survey respondents).

The current working environment is here to stay indefinitely and for organizations to continue doing business they need a more sustainable approach to security. Attackers are stepping up all forms of exploits against remote workers, with ransomware continuing to be highly evident. People, process, and technology are all crucial components of the security controls that are needed to prevent, detect, and respond to security incidents and breaches across all environments. Omdia’s ICT Enterprise Insights, undertaken during the early days of the pandemic, show that the management of security, identity, and privacy is way in the lead as a top three priority, highlighted by well over half of the survey respondents.

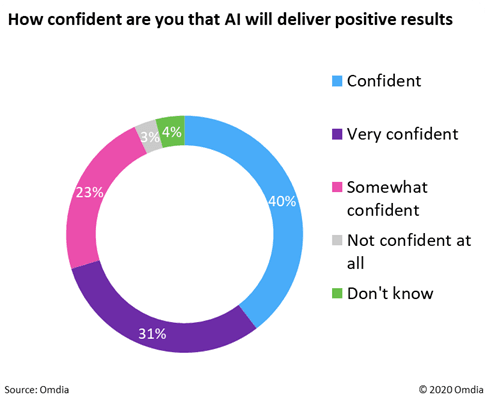

Amid market disruption, optimism remains for AI platforms and intelligent automation

Despite looming concerns among enterprise AI practitioners regarding scalability, speed-to-market, privacy, security, safety, and responsibility, there continues to be drive in AI investment with focus turning to rigorous technologies such as MLOps and AI governance for more operational oversight. Under the rubric of the COVID-19 pandemic, enterprise AI practitioners are turning their attention away from speculative projects to instead focus on more tactical concerns that promise corporate stability and agility. Projects without a clear and immediate ROI will be put on temporary hold, with new projects capable of driving value across disparate departments and use cases will take precedence. This shift in perspective will require supportive investments in technologies and best practices capable of resolving several nagging issues regarding the repeatability, scalability, and surety of all in-house ML projects. In response to the first two issues, technology providers are building lifecycle-complete solutions capable of operationalizing the full machine learning (ML) model lifecycle. The goal of these MLOps platforms is to help enterprise AI practitioners' speed in time to market and increase the number of projects they can carry at any given time. Resolving the third issue regarding security (or the trust companies have in their deployed AI projects), will require far more than a better way of moving ML models from development into production. Omdia anticipates, therefore, that AI technology vendors will seek to partner with customers to better understand and control the multifaceted interplay between human, data, and algorithm. Initial investments in removing bias from data and algorithms, for example, will evolve to address more complicated issues such as corporate responsibility, liability, governmental oversight/compliance, and ethics.

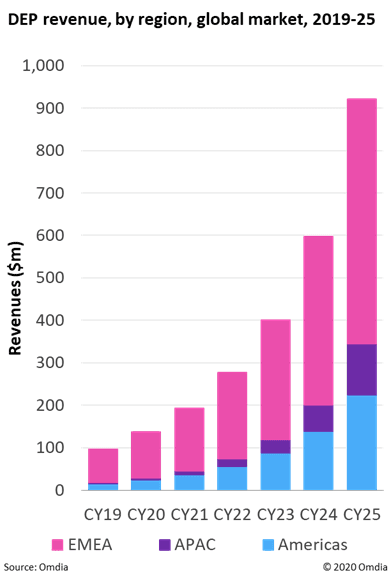

IoT DEPs enable sharing, reuse, and monetization of data IoT DEPs (data exchange platforms) enable data exchange and monetization and represent the next stage in the evolution of the IoT market. 2021 will mark a key inflection point for global IoT DEP market growth. Europe is leading in IoT DEP market development because of the large share of EU-based DEP providers, key EU-based DEP standardization work, public funding for IoT DEP-related projects (such as GAIA-X), and the work of IoT DEP-relevant industry organizations based in the EU, such as the FIWARE Foundation and the IDSA.

The IoT data exchange market opportunity is broad-based, but there are four clear early adopter market segments, which are seeing strong initial strong traction. These are: connected cars, smart cities, industrial automation, and precision agriculture. Vendors offering IoT DEPs include both “pure play” firms, such as Chordant, Dawex, OpenDataSoft, Terbine, and Umbrellium, as well as diversified tech vendors, including AWS, HERE, HPE Pointnext, and Schneider Electric.

IoT DEP standardization efforts have focused on creating extensible core “foundation ontologies” that can be extended to specific market segments later by market participants themselves, as needed, and according to what’s useful and practical. Omdia considers the two primary standardization efforts relevant to IoT data exchange to be ETSI ISG CIM and W3C Web of Things.